Another exciting week is over, and markets participants are still divided on how we will continue from here. The headlines are full of mixed messages, some stating that „markets will drop 15 - 20% soon“, while others see this phase as the start of a new bull run.

I expected some downward impulses last week, but markets proved me wrong:

DAX

DJIA

S&P 500

Nasdaq Composite

S&P MidCap 400

Russell 2000

15922,27 34,098.16

4,169.48 12,226.58 2,490.40 1,769.00

70,11 289.20 35.96 154.13 -8.42

-22.52

↑

↑

↑

↑ ↓ ↓

DAX

DJIA

S&P 500

Nasdaq Comp.

S&P MidCap 400

Russell 2000

15922,27 34,098.16

4,169.48 12,226.58 2,490.40 1,769.00

70,11 289.20 35.96 154.13 -8.42

-22.52

Sources: Yahoo Finance, boerse.de

In the end I got out with a few points of profit, which again shows us how important Stop-Loss Orders are :)

1) Earnings reports

Alphabet, Microsoft, META and Amazon reported strong numbers and lifted the markets higher. So far approximately 50% of S&P 500 companies have reported actual results, with the majority of those companies reporting a positive EPS and revenue surprise. The blended earnings of the S&P 500 is at -3,7%. An interesting and detailed breakdown of the numbers can be found here: https://www.factset.com/earningsinsight

The earnings for the upcoming week:

2) Banking crisis

While you and I enjoy our weekends, the employees at the FDIC are busy assessing bids for First Republic Bank in an urgent rescue attempt. Last week First Republic disclosed that the amount customers had withdrawn in March was at around $ 100 billion. 11 Banks pumped $ 30bn into the bank to stabilize it back then.

According to BBC.com and Reuters, JP Morgan and Bank of America are among those who were asked for a bid. If no buyer can be found, the FDIC could step in and guarantee all deposits like it did with Silicon Valey and Signature in March, to prevent a bank run.

First Republic stock has fallen 97% this year so far, with a plunge of 43% last friday and several trading halts due to volatility reasons.

3) Geopolitical situation

Last week saw some activity on the diplomatic front with China trying to position itself as a mediator in the Russian-Ukraine war, while US administration tried to strengthen its bond to the Phillipines, an important ally in case of a military conflict due to its position in the Pacific. Meanwhile foreign companies face more pressure in China, as the government expanded the scope of the law about espionage, giving authorities power to gain access to all electronic data. The law covers „documents, data, materials and items related to national security“, without clearly defining what „national security“ means.

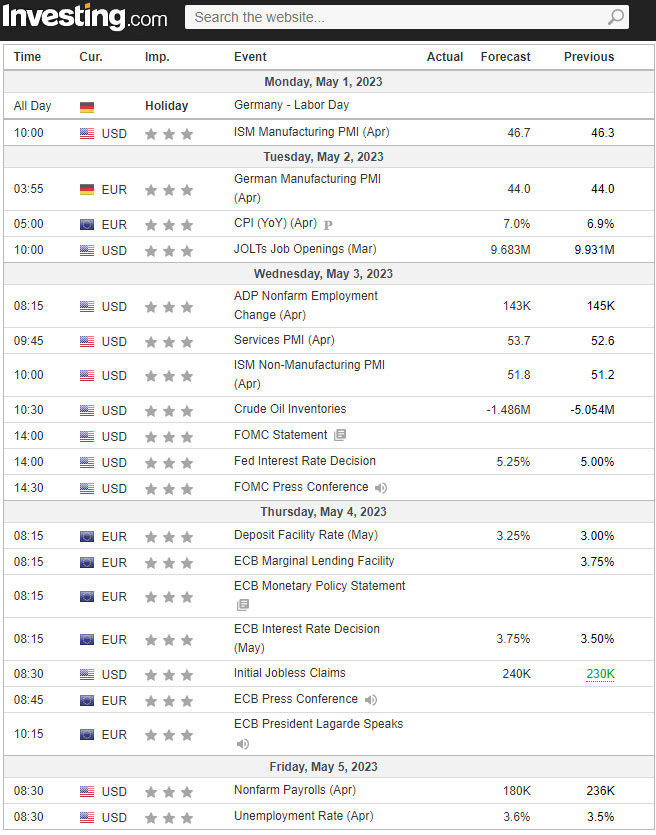

4) Economic Calendar

Last week GDP came in lower than expected with 1,1% YoY (+2.6% in Q4 2022; +3.2% in Q3 2022). PCE (FOMC's primary measure of inflation!) showed a still too high inflation with +4,6% from one year ago.

This week the FED will start their two-day policy meeting on May 2nd, with their interest rate decision on May 3rd: the FED is expected to raise rates by 25bps, bringing the target range to 5.00-5.25%.