Last week the markets moved lower for most of the week, with a rally on Friday easing some of losses and erasing those of Nasdaq. The FED raised rates as expected and hinted at a pause in increases. The reemerged banking crisis, with the takeover of First Republic Bank’ s assets by JP Morgan over the weekend, led to some turbulence in the markets, especially some regional banks: PacWest dropped 50.6% on Thursday, but led the rebound of US regional-banking stocks on friday.

DJIA Nasdaq S&P DAX Cr. Oil Gold

33,674.38

12,235.41

4,136.25

15,961.02

71.34

2,017.4

-423.78 8.83 -33.23 38.64 -5.44

26.7

-1.26 %

0.07 %

-0.80 %

0.24 %

-7.63 %

1.32 %

Source: Yahoo Finance

Source: TradingView, DJIA 1h

1) Earnings reports

The week had more earnings releases, with very mixed numbers. The much anticipated release by Apple showed higher profits on Iphone sales, with a lower revenue. The release on Thursday evening definitely gave the markets a positive impulse for Friday.

The FED increased the the rate by 25bps, as expected, and hinted to a possible peak in the monetary tightening cycle. FED Chair Powel nevertheless kept all options on the table and made clear that a decision to pause has not been made yet. A lot of market participants speculate on decreases beginning in the second half of the year, but so far numbers don’t really support that idea in my opinion: although inflation is still way above the 2% target and as long as we don’t see lower numbers, the rates will be kept up.

The US labour market remains strong, as U.S. nonfarm payroll jobs increased by 253,000 in April (above cons. est. of 185,000). Small signs of softening were weekly jobless claims trending higher and job opening rates moving lower. Nevertheless it remains tight and the FED expects the unemployment rate to peak at 4,6% in the future.

The FED still sees the banking sector as healthy, and it stands ready to provide liquidity to the sector together with the government. From a traders perspective, however, any „bad“ news from the banking sector could lead to higher volatility in the markets and I will definitely keep an eye on that this week.

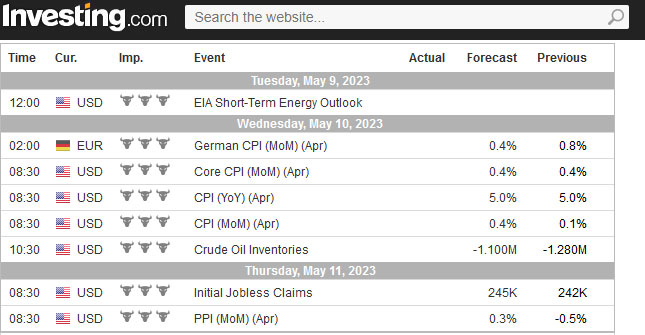

3) Economic Calendar

The most important events will be German and US CPI data on Wednesday, US PPI data and Initial Jobless claims on Thursday